What are closing entries with examples?

Temporary accounts are closed or zero-ed out so that their balances don’t get mixed up with those of the next year. All of Paul’s revenue or income accounts are debited and credited to the income summary account. This resets the income accounts to zero and prepares them for the next year. Temporary accounts can either be closed directly to the retained earnings account or to an intermediate account called the income summary account.

Step 3: Close and Credit

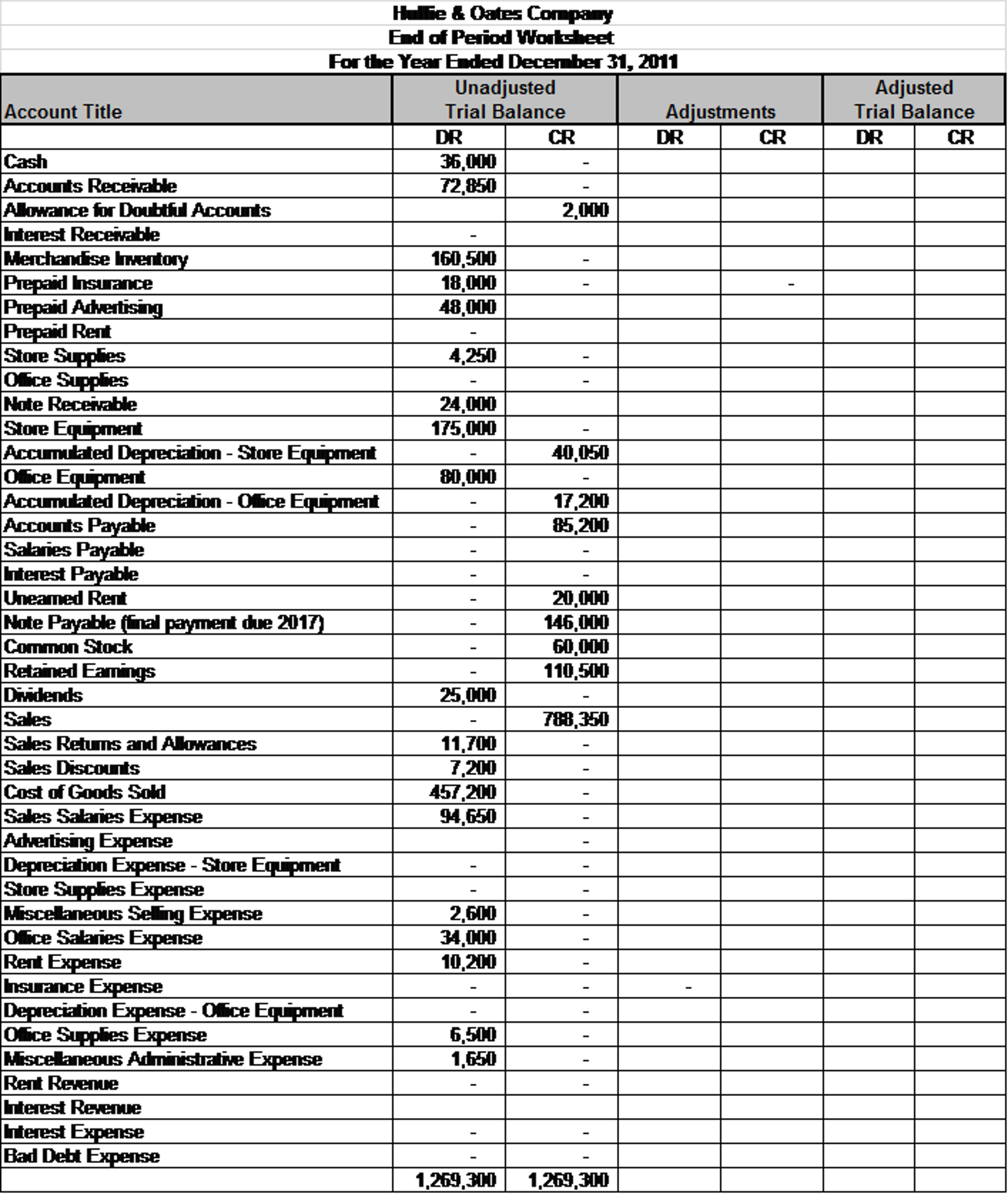

The trial balance is like a snapshot of your business’s financial health at a specific moment. It lists the current balances in all your general ledger accounts. In this case, we can see the snapshot of the opening trial balance below. In order 7 ways to improve your accounts receivable collections to produce more timely information some businesses issue financial statements for periods shorter than a full fiscal or calendar year. Such periods are referred to as interim periods and the accounts produced as interim financial statements.

Journalizing and Posting Closing Entries

Remember the income statement is like a moving picture of a business, reporting revenues and expenses for a period of time (usually a year). We want income statements to start every year from zero, but for accounts like equipment, debt, and cash accounts—reported on the balance sheet—we want to keep a running balance from the beginning of the business. Closing entries are performed after adjusting entries in the accounting cycle.

Which of these is most important for your financial advisor to have?

A company will see its revenue and expense accounts set back to zero, but its assets and liabilities will maintain a balance. Stockholders’ equity accounts will also maintain their balances. In summary, the accountant resets the temporary accounts to zero by transferring the balances to permanent accounts. Closing entries are journal entries used to empty temporary accounts at the end of a reporting period and transfer their balances into permanent accounts.

Examples of Closing Entries

- Whether your company uses single or double-entry accounting, you will need to ensure the proper method of opening and closing journal entries happens at the designated time.

- The eighth step in the accounting cycle is preparing closing entries, which includes journalizing and posting the entries to the ledger.

- Well, dividends are not part of the income statement because they are not considered an operating expense.

- Thebusiness has been operating for several years but does not have theresources for accounting software.

- To close that, we debit Service Revenue for the full amount and credit Income Summary for the same.

Therefore, the beginning balance of these accounts can be taken from the previous period closing account balances. Journal entries are an essential part of the accounting process for any business. Whether your company uses single or double-entry accounting, you will need to ensure the proper method of opening and closing journal entries happens at the designated time. Why was income summary not used in the dividends closing entry? Only income statement accounts help us summarize income, so only income statement accounts should go into income summary.

Recording a Closing Entry

The eighth step in the accounting cycle is preparing closingentries, which includes journalizing and posting the entries to theledger. Reporting cycles are an essential part of the accounting process. The cyclical reporting of accounting periods can span monthly, quarterly, and annual time frames. However, when it comes to opening and closing accounts, this typically happens on a yearly or monthly basis, depending on the type and size of the company. ‘Retained earnings‘ account is credited to record the closing entry for income summary. Expense accounts have a debit balance, so you’ll have to credit their respective balances and debit income summary in order to close them.

Our discussion here begins with journalizing and posting the closing entries (Figure 5.2). These posted entries will then translate into a post-closing trial balance, which is a trial balance that is prepared after all of the closing entries have been recorded. The closing journal entries example comprises of opening and closing balances. Opening entries include revenue, expense, Depreciation etc., while closing entries include closing balance of revenue, liability, Depreciation etc. After the posting of this closing entry, the income summary now has a credit balance of $14,750 ($70,400 credit posted minus the $55,650 debit posted).

Whenyou compare the retained earnings ledger (T-account) to thestatement of retained earnings, the figures must match. It isimportant to understand retained earnings is not closed out, it is only updated. RetainedEarnings is the only account that appears in the closing entriesthat does not close. You should recall from your previous materialthat retained earnings are the earnings retained by the companyover time—not cash flow but earnings. Now that we have closed thetemporary accounts, let’s review what the post-closing ledger(T-accounts) looks like for Printing Plus.

Each accounting period’s data must be contained within the designated time frame in order to accurately depict the financial standings of the company. ‘Total expenses‘ account is credited to record the closing entry for expense accounts. Permanent (real) accounts are accounts that transfer balances to the next period and include balance sheet accounts, such as assets, liabilities, and stockholders’ equity.